Gold has been historically considered as an important asset class mainly for three reasons:

• Hedge against inflation

• Adds stability to the investment portfolio

• Asset Allocation avenue

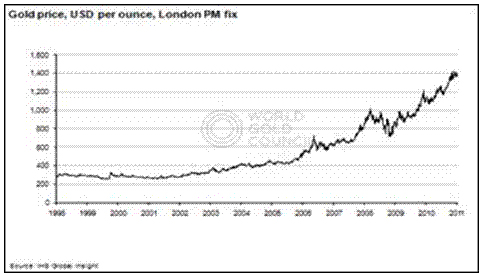

And as an asset class, gold over the year has shown a secular uptrend. In 1971, the price of gold was about U.S. dollar 32 an ounce and today (i.e. on February 28, 2011) it is U.S. dollar 1,383.50 an ounce –which indicates that price of gold has gone up by 43 times over the last 40 years. Even in the last 13 years (i.e. since Jan 1998) as depicted in the chart hereunder, till February 18, 2011 gold prices have appreciated by whooping 380% (on an absolute basis).

Whenever, Governments and central banks of the world exhibit financial exuberance, thus raising chances of economic turmoil in the form of ballooning fiscal deficit, inflationary situation, slowing economic growth rate, high unemployment rate etc; smart and prudent investors prefer taking refuge under gold which makes this asset class look bold. And when all such downbeat economic data is released, if the central banks the world resort to printing more money (in order to take the economy out of the woods), it in effect puts downward pressures on the dominant currency – such as the U.S. dollar, which in turn fuels the upward movement of gold.

In the year gone by (in 2010) too, Euro zone - especially Greece, Ireland and Spain continued to experience burgeoning debt crisis. The U.S. economy too for the major part of the year suffered the pain of high unemployment rate, low economic growth rate and low consumer confidence; which eventually led to stimulus package being announced in the form of QEII, in an attempt to revive their (U.S.) economy. In India the political uncertainty caused due to several scams such as the 2G spectrum scam, Adarsh Housing Society Scam and the housing finance scam, also led to the precious yellow metal becoming bolder (rose by 23%). Moreover, gold merchants also maintained elevated stock levels, as physical demand also remained robust due to several auspicious muhuraths during the year.

Talking about the year ahead, the U.S. economy is still on a stimulus (paper driven due to QEII announcement), which is leading to depreciation in the value of the dominant currency – the U.S. Dollar, which in turn is keeping an upward bias on the prices of gold (gold prices and the U.S dollar are inversely related to each other). Moreover interestingly post the QEII announcement, commodities as an asset class is witnessing a sudden upward rally, which is also attracting investor’s attention to the precious yellow metal.

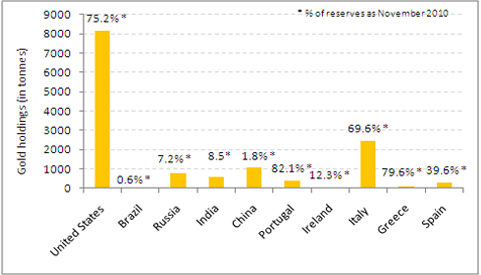

In the Euro zone too – Greece, Ireland and Spain are continuing to experiencing a "debt overhang", thus revealing the fact that they are yet not out of the woods. In fact knowing that the economic recovery is wobbly, most economies led by the U.S. and the Euro zone ones are maintaining elevated levels of gold reserves too (as revealed by the chart below), in order to hedge the risk of an economic breakdown.

(Source: World Gold Council, PersonalFN Research)

It is noteworthy that even a natural disaster like an earthquake, Tsunami, floods etc has a positive impact on the prices of gold. Take the case of Japan; after an earthquake and Tsunami occurring and causing damage to mankind and industry, gold prices have displayed an upward bias due to the fact that it acts as a hedge against the economic loss faced by people, industry and the Government.

Thus taking into account the fundamentals for gold presented above and cashing on the opportunities of wealth creation available with this asset class; at present the Indian mutual fund industry is seeing a new breed of fund called "Gold Savings Fund" or "Gold Fund", being launched by fund houses such as Reliance Mutual Fund and Kotak Mutual Fund in the market.

What is a Gold Savings Fund?

A "Gold Savings Fund" (also known as a "Gold Fund") is generally Fund of Fund (FoF) scheme which invests its corpus into an underlying Gold ETFs and benchmarks its performance against the physical prices of gold. Hence by doing so, it attempts to provide returns that closely correspond to the returns of its underlying Gold ETFs.

Even though "gold saving funds" are passively managed, the most wonderful thing about them is that, they provide you the opportunity to invest in gold without really having to worry much about how to store it physically, since the units (your holdings in gold) are allotted in a paper form. Moreover, such a fund also provide you with the convenience of a Systematic Investment Plan (SIP) as well as lump sum investments, but without having you to open a demat account to avail its benefits (which is unlike Gold ETFs).

Since SIP is a special feature of a "gold savings fund", it provides you with the following advantages:

• Convenience

• Discipline while investing,

• Rupee-cost averaging

• Compounding

Also since holding a demat account is not necessary, you do not have to incur the following charges thus making it a cost effective investment proposition.

• Annual maintenance charge for demat account

• Delivery brokerage charges

• Transaction charges (while investing in demat mode)

Moreover liquidity too is generally not restrained by the fund, as you can subscribe and redeem units on all business days directly from the AMC (while purchase and sale of gold ETFs depends upon the liquidity on the exchange).

What’s the Asset Allocation?

Gold savings fund invest a dominant portion (95% - 100%) of their assets in the underlying Gold ETFs, while upto 5% of their assets are held in debt and money market instruments.

|

|

|

Units of "Gold Savings Fund" |

95% - 100% |

Medium to High |

Reverse repo and / or CBLO and / or short-term fixed deposits and / or Schemes which invests predominantly in money market securities or Liquid Schemes* |

0% - 5% |

|

It is noteworthy that the underlying Gold ETFs (which the gold savings fund invests in) invests in physical gold which shall be of fineness (or purity) of 995 parts per 1000 (99.5%) or higher.

What about the tax implications?

On the taxation front too as per the present tax laws (Income Tax Act, 1961), investment in a gold savings fund enables you to avail the benefit of long-term capital gains tax, after the period of one year of its holding. However, any sale of the fund before the period of 1 year would attract short-term capital gains tax.

It is noteworthy that at present for investment in physical gold, the benefit of long-term capital gains tax is available only after the completion of period 3 years of the asset’s holding.

|